Preview of week starting 27June2022

Public Holidays (China, Hong Kong & USA)

01 Jul 2022 - Hong Kong Public Holiday

Earnings Calendar

The charts below are from Earnings Whispers:

Personally, I am looking at Nike, Trip, Micron and meme stock Bed Bath & Beyond.

#earnings $NKE $TRIP $MU $BBBY

Source is @eWhispers

Now, let us look into Micron in detail:

From the above, the market is expecting an EPS of 2.46 and revenue of $8.68B from its 30 June 2022 earnings. Will Micron be able to continue its reversal? Let us monitor this closely.

News Summary

Sri Lanka no longer has money to buy fuel. Laos has defaulted on their bonds.

Secretary-General Warns of Unprecedented Global Hunger Crisis, with 276 Million Facing Food Insecurity, Calling for Export Recovery, Debt Relief.

Sixteen companies and thousands of Aussie jobs are gone in six months as the collapse crisis rages on. Australia is in the grips of a construction industry crisis, with 16 firms and countless jobs disappearing – and it’s only going to get worse.

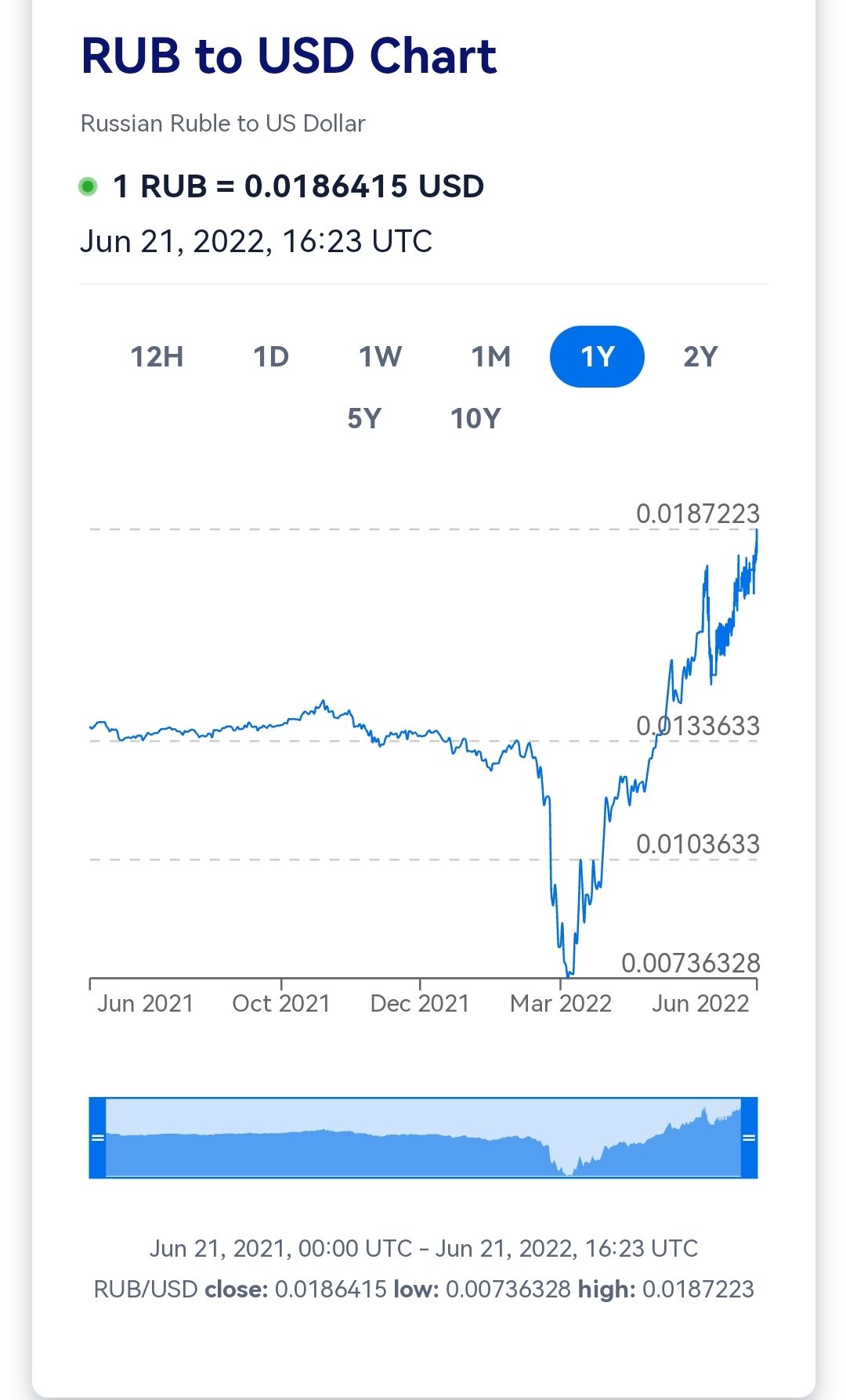

China and India buy oil from Russia as the war drags on as per news from Nikkei on 8 Jun 2022 news article. China and India buy more Russian oil, blunting Western sanctions. Both countries take advantage of discounts as buyers disappear.

Russian Ruble hits a recent all-time high since the recent dip due to sanctions in March ... India and China buying their oil played a part over here.

Economic Calendar

For this week, there are several important indicators which will render a better understanding of global economic health.

With China being one of the world's factories, their Manufacturing PMI (Jun) & Caixin Manufacturing PMI (Jun) will be important to provide an understanding of both global demand and supplies. Though China has to enforce lockdown in several major cities, they have since re-opened and we can expect the manufacturing to pick up. However, if there are lesser orders, this can also be seen in the indices. The figure may be "misleading" because it can be due to a mixture of both re-opening from lockdown and fulfilling backlog orders. Thus, we are unable to put a stronger pulse on global demand which may be waning in lieu of the higher inflation.

For the US, let us continue to monitor cruise oil inventories as this will spell both the market sentiment for both demand and production. With oil, a product of the upstream, a larger than expected drawdown can imply that consumer demand remains high.

CB Consumer Confidence is also a key indicator as this implies the level of consumption. As confidence drops, it is likely that most families will look to tighten their spending or channel more into savings in anticipation of a weakening economy.

Pending home sales are also a good thermometer for the red hot real estate. With the increase in mortgage rates, we can expect this to drop are homes become more expensive with the interest rate hikes. Families who were unable to find homes before the recent rate hikes may continue to find homes out of their financial reach. With the expected rate hikes to bring down the inflation, getting a home can be beyond the budget of more and thus, resulting in some cooling off. In a recent news article, there were billionaires still buying up luxury homes on West Coast but this does not reflect the other tiers.

The initial jobless claims should increase with more companies announcing retrenchment. This could lead to the start of a recession. Retrenchment can lead to a recession. Retrenchment > unemployment increase > consumption decrease > earnings decrease > GDP decrease > repeat

During a recession, the economy struggles, people lose work, companies make fewer sales & the country's economy declines.

Lastly, the US ISM Manufacturing PMI will reveal the status of the manufacturers based on their orders, back orders, inventories and so forth. A higher than expected is usually bullish for the market and economy.

Market Outlook

Using the 1D chart (TA), the Stochastic indicator shows an up trend for S&P and we can expect MACD to bottom-up (implying an uptrend). Let us watch the support (3640+/-) and resistance region (4150+/-). As per previous posts, support and resistance are not a singular price but rather a price range.

My investing muse:

Oil continues to send inflationary ripples into the rest of the economy as the Ukraine war drags on. Despite the sanctions, few of us realised that the Russian Rubles has recently hit a 5-year high thanks to other buyers of their products.

However, with Russia producing 40% of the world's fertilizer, the impact on agricultural production will soon be realised. With climate change and extreme weather continuing to taunt the agricultural and livestock, the food crisis is likely to hit regionally. If Singapore has to secure eggs from Poland, understand that it is not an achievement but it amplifies the food & supply chain crisis that we face. UN has just advised that 276 million could face

20 million tons of grain remain stuck in Ukraine, needed by many as food or livestock feed. At this point, the fallout of Ukraine has spread to fuel, food, energy and supply chain crisis. With climate change and weather, extremities continue to hit different parts of our world, food security is under threat for many.

While the technical indicators for S&P 500 1D chart point to a rally this week, let us remain cautiously hopeful as I am expecting a recession to follow. Buy great companies at good discounts, hold and monitor regularly. If their fundaments are affected over a prolonged season, review and always have an exit plan.

Spend within our means, invest with what we can afford to lose. Set aside some "cash for crash"

Comments

Post a Comment